When working in a subscription world where you collect monthly payments from customers for products or services that you are offering, you are going to need a way for those customers to pay you. The monthly recurring revenue that you are invoicing to customers needs to be collected, and a great way to accomplish this first task is by accepting credit cards as a form of payment.

Visa, Mastercard, Discover, and American Express are the four major brands of credit cards that are accepted globally, either through Point-Of-Sale (POS) terminals or through eCommerce sites like Amazon, Apple, and Wayfair. You must accept credit and debit cards in your business if you want to have a successful customer base and company. There are also other newcomers to this trend in the digital world like Payal, Venmo, and Zelle.

We are going to explore how to accept the four major brands and also learn more about digital payments.

How Does Credit Card Processing Work?

Some think this is a very straightforward process: you swipe your customer’s card, and two days later, money shows up in your bank account.

Credit card processing is more complicated than that.

With every swipe made, there is a complex web of businesses working behind the scenes to eventually have that deposit made into your bank account, and in order to accept credit or debit cards, you need to get acquainted with the world of credit card processors.

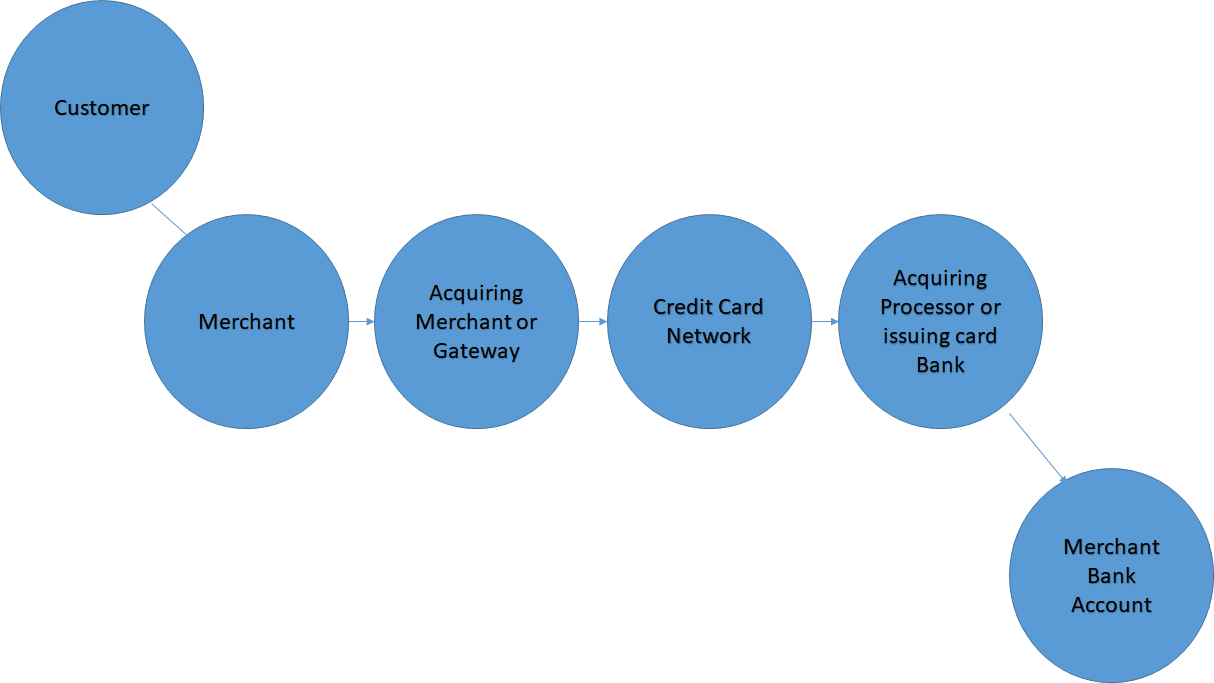

While this process typically occurs in a matter of seconds, there are lots of players involved. Here is the complete five-step process for credit card processing from the customers to the merchant:

- Cardholder – The customer is the first transactor in the process using either a credit or debit card to start the credit card processing process.

- Merchant – This is your business that sold the product or service to the cardholder.

- Acquiring Merchant or Gateway – This is where the authorization of the credit card is completed. It is the first outside party that looks at the charge to determine if the cardholder’s card is valid for completing this transaction. The merchant can be a bank or a gateway. Vendors in this space include Cybersource, Authorize.net, and Stripe.

- Credit Card Network – These are the companies that take the credit card details from the gateway and send the data to Visa, Mastercard, Discover, or American Express for validity and finalization. This is done through the Interchange Network, which involves forwarding of the payment authorization from the gateway to the issuing cardholder bank and back to the processor.

- Acquiring Processor – The processor usually provides the Point-Of-Sale (POS). For example, where you insert your card at your local grocery store or Starbucks would be considered the POS. They are the ones in the end who pay you for that transaction. Major processors in the United States that take global payments are WorldPay/FIS, Chase Global payment, and Elavon.

Merchant Pricing Models

When choosing a provider for your merchant processing, be aware that there are different pricing models provided by the merchants.

There are two common pricing models:

- Percentage Per Swipe – For every swipe of the card, the merchant will charge you a flat overall percentage for every dollar collected. The interchange fees for the credit card networks will be included in the overall percentage used. The average percentage charged is between 2.90% and 4.50%, depending on volume.

- Cost Per Swipe – The other main model is to be charged a small fee per-swipe, and then have the interchange fees over top of that. You would pay 10 cents a swipe plus fees.

Interchange Merchant Fees

Interchange rates are the rates charged by VISA, Mastercard, Discover, and American Express, and they are the same rates charged to every merchant. These fees are public information and are non negotiable when looking at singing a contract with a new merchant processor.

The reasons why these costs exist is to help the cards brands pay for fraud risks and the handling costs of the transactions. These interchange rates will vary depending on:

- The card used

- The bank who issued it

- If it is a debit or credit card

- If the card is present in the transaction or not

- The type of business accepting the card

- The amount of the transaction

Every factor that increases the risk of the charge not being successful increases the rate charged. For example, debit cards are charged a cheaper rate than credit cards, since the money is in that person’s bank account when swiped. Card present means the card is more real and exists over a card not present during the transaction, and therefore charged a cheaper interchange rate.

What Other Fees are Included With Credit Card Processing?

There are six other fees you need to be aware of when setting up credit card processing:

- Dues and Assessments – The processor needs to collect a fee, so they can pay VISA or Mastercard for the right to be a processor. These are different than interchange fees and are usually based upon the volume of sales that the merchant has in a month.

- Processor’s Fee – This is based upon the pricing model above, and there are two options here: the all-in rate or the per-swipe fee. If you have a high volume of transactions like most subscription based companies do, the per-swipe rate is the best way to go.

- Gateway Fee – If you use a separate gateway that your merchant processor does not provide, you will need to pay them a per-swipe fee as well. This is very common if you have Authorize.net or Cybersource as your gateway, and a bank as your merchant processor.

- POS Costs – You might have to rent your POS machines and pay a fee for each one.

- Chargebacks – This is the fee incurred when a customer issues a chargeback against the service or product you provided.

- Monthly Service Fees – This can be a statement fee or a fee for not meeting your monthly minimums in your contract. You will want to be sure you know what your average transaction size and volume will be when negotiating your merchant processor contract.

Other Ways for Customers to Pay

Some people call these digital wallets, digital payments, or even mobile payment systems. The leaders in the digital wallet space are Paypal, Venmo, Apple Pay, and Zelle.

As a merchant selling goods and services, be sure you are able to accept as many forms of payments as you can. You never want to turn a potential customer away due to not providing their preferred payment method.

This growing trend is not going to stop, and you will want to make sure your eCommerce and POS machines are able to accept either through your merchant processor or through your eCommerce store.

Struggling to Scale Your Business? Find out Why Outsourcing Managed Web Services is Better for Your Business

[ad_2]

Source link